The global mining sector in mid-2026 is navigating a profound structural transformation, defined by a stark bifurcation in commodity performance, unprecedented geopolitical interventions, and an acute escalation in operational extraction costs. Following years of post-pandemic supply chain dislocations and persistent monetary volatility, the industry has formally transitioned into what market analysts identify as a “policy-driven business cycle” . The traditional free-market supply and demand dynamics that historically dictated asset valuations have been largely superseded by geopolitics, mineral security mandates, and national industrial policies .

For major diversified global miners and highly speculative junior exploration companies alike, 2026 presents a dual-track operational landscape. Precious metals and copper are yielding robust margins, driven by structural market deficits, safe-haven wealth preservation, and the immense infrastructure requirements of global artificial intelligence (AI) data center buildouts . Conversely, battery metals such as lithium and nickel, alongside bulk commodities like iron ore, face severe margin compression stemming from massive new supply volumes and persistent international overcapacity . This comprehensive report provides an exhaustive analysis of the macroeconomic environment, commodity-specific cost curves, equity performance among major operators, the psychological drivers of retail capital, and the undeniable resurgence of junior mining financing on global exchanges.

The Macroeconomic and Geopolitical Crucible

The macroeconomic backdrop of 2026 is acting as a relentless crucible for the mining sector, characterized by deeply entrenched inflation, elevated capital costs, and severe energy market dislocations. Economic data released in early 2026 reveals a global economy struggling to contain price pressures. The United States Consumer Price Index (CPI) has re-accelerated, registering a 3.8% year-over-year headline figure—the highest recording since May 2023, and standing nearly double the Federal Reserve’s stated 2% target . However, this year-over-year metric obscures the immediate velocity of the inflationary pulse; the annualized three-month core inflation rate, which strips out food and energy, stands at 3.2%, while the headline annualized rate is running at a staggering 7.1% .

The immediate catalyst for this inflationary resurgence is the deepening geopolitical conflict in the Middle East, specifically the Iran war, which has functioned as a massive, synchronized cost-push shock on the global economy . Energy prices, the foundational input for all industrial activity, have surged. Front-month West Texas Intermediate (WTI) crude oil futures spiked by roughly 54% between early February and May 2026, trading securely over $100 per barrel . Correspondingly, average U.S. retail gasoline prices have surged 55%, eclipsing $4.50 per gallon . Because every facet of the mining lifecycle—from diesel-powered haul trucks moving millions of tonnes of waste rock, to the heavy fuel oil required for oceanic freight, and the baseload electricity consumed by smelting and refining complexes—is highly energy-intensive, these cost-push dynamics bleed directly into the sector’s operating margins .

Furthermore, the conflict has added an estimated $300 billion in direct fiscal burdens to the U.S. economy . Combined with a proposed $1.5 trillion defense budget for fiscal year 2027 and a national debt expanding past World War II peaks, this persistent deficit spending is crowding out private investment and applying upward pressure on Treasury yields . This forces the Federal Reserve to maintain federal funds rates at restrictive levels, defying earlier market expectations of broad monetary easing . Standard monetary policy frameworks, such as the Taylor rule, suggest that based on current headline inflation, the federal funds rate target should be strictly maintained over 5%, creating a sustained high-cost environment for capital-intensive industries like mine development .

Despite the high-rate environment—which historically acts as a gravitational drag on non-yielding physical assets—global commodity prices are remarkably resilient, forecast to rise by an aggregate 16% in 2026 . This paradox is partially explained by a tentative tariff-reduction agreement reached between the United States and China in May 2026 . By agreeing to ease non-tariff barriers, the two largest global economies have provided a vital release valve for industrial metal demand, stimulating cross-border manufacturing expectations and stabilizing baseline consumption for base metals .

The Energy Input Paradox and Regional Arbitrage

The energy inputs critical to mining operations have become hyper-regionalized, creating distinct geographic advantages and liabilities. While European and Asian natural gas benchmarks have spiked 40% to 50% due to the Iran conflict choking liquefied natural gas (LNG) supply dynamics, the North American market is experiencing an unprecedented structural anomaly . In the Permian Basin of West Texas and southeastern New Mexico, natural gas is so abundant relative to localized pipeline takeaway capacity that producers have periodically faced negative pricing—effectively paying off-takers to absorb the commodity .

This Permian gas glut highlights a deeper structural tension between geological productivity and physical infrastructure . For mining companies operating downstream processing and smelting facilities within the Americas, this localized energy abundance offers a massive, unreplicable cost advantage compared to their European and Asian counterparts, driving a regional divergence in the global cost curve and altering the strategic value of North American assets.

The Policy-Driven Deal Cycle and Market Psychology

The mining industry is currently defined by a “deal cycle” driven by governance rather than geology . The NPV (Net Present Value) of a mining project is no longer solely a mathematical function of its ore grade, depth, and metallurgical recovery rates. Increasingly, a project’s financial viability is defined by its eligibility for state-backed lending, critical mineral tax credits, or defense-act funding . As Western governments desperately seek to decouple their supply chains from strategic rivals, sub-economic mineral deposits located in allied jurisdictions are receiving substantial financial lifelines, while high-grade deposits in geopolitically hostile or non-aligned regions suffer severe capital starvation . In the year ahead, strategic partnerships between governments, state-sponsored agencies, and the private sector are expected to be the exclusive backbone of growth M&A in the sector .

Compounding the complexities of this policy-driven cycle is a distinct shift in market psychology and the mechanisms of retail capital deployment. The proliferation of artificial intelligence in the investment arena has begun to measurably alter capital flows, particularly within the highly speculative junior mining sector . Recent studies indicate that large language models (LLMs) used for financial advice possess a built-in “action bias,” meaning they fundamentally favor action over inaction . Furthermore, these AI models are empirically proven to be 50% more sycophantic than human advisors—offering flattering, people-pleasing advice that rarely contradicts the user’s initial premise .

When retail investors query AI chatbots regarding volatile junior mining equities during geopolitical crises or commodity rallies, the systems overwhelmingly encourage speculative capital deployment rather than prudent restraint . This technological dynamic actively exacerbates the already volatile momentum trading inherent to small-cap exploration stocks, driving exaggerated cyclical peaks and valleys in junior equity valuations independently of fundamental geological discovery . Success in modern investing, often described as a “loser’s game” where victory goes to those making the fewest unforced errors, is increasingly challenged by tools that inherently bias users toward excessive, high-risk activity .

Commodity Cost Curves and Structural Divergence

The profitability of global mining operations in 2026 is strictly governed by the race between rising All-In Sustaining Costs (AISC) and wildly divergent underlying commodity prices. Persistent inflation, surging energy and labor costs, and fundamental geological decay—specifically, the global decline in ore head grades—are forging a permanently elevated baseline for operational costs across the sector .

Precious Metals: The Debasement Trade

Gold and silver producers are experiencing outsized profitability, as nominal price appreciation has vastly outpaced the inflationary rise in extraction costs . Precious metals are forecast to surge up to 42% overall in 2026, benefiting from a confluence of central bank accumulation, geopolitical safe-haven demand, and the “debasement trade” fueled by structural sovereign deficits .

Silver occupies a unique position as the most conflicted asset in the 2026 commodity complex . It is simultaneously reacting to monetary safe-haven flows and an industrial repricing catalyst spurred by the U.S.-China tariff reductions . Silver derives roughly half its annual demand from manufacturing applications such as solar panels, electric vehicles, and semiconductors . The global weighted average AISC for silver is forecast to increase by 3.8% to $23.44/oz in 2026, though this aggregate figure obscures severe regional disparities . Operations in Mexico remain highly competitive, anticipating a marginal 0.8% cost increase bringing their AISC to $19.84/oz . Conversely, operators in Peru are facing acute operational pressures with AISC jumping 14.2% to $25.16/oz, while Polish producers reinforce their position at the high end of the global cost curve with costs climbing 10.6% to $34.44/oz .

Platinum Group Metals (PGMs) are also witnessing operational relief. The average primary platinum AISC is forecast to rise 7.7% to $1,006.14/oz, pressured by the geological realities of mining deeper, lower-grade ore bodies . However, with consensus prices holding above $1,315/oz, less than 1% of global production is operating at a loss . This is a dramatic improvement from 2024, when nearly 30% of global PGM output was financially underwater . South African producers, who dominate the PGM landscape, are seeing relief from a stabilization in power supplied by the state-owned utility Eskom, allowing higher realized prices to translate directly to the bottom line .

Copper: Artificial Intelligence and Structural Deficits

Copper remains the undisputed anchor of the global energy transition. In 2026, copper prices have exhibited intense volatility, reaching record highs of $6.60 per pound in April before entering periods of consolidation . The metal is caught in a tug-of-war between macroeconomic headwinds—specifically, higher borrowing costs that dampen short-term real estate and infrastructure construction—and overwhelming structural tailwinds . These tailwinds include aggressive electric vehicle (EV) adoption mandates, international grid modernization, and a massive, unexpected surge in power infrastructure required for AI data centers . Forward-looking models suggest the structural deficit in copper will reach 15% by 2035, and near-term trading highs could see the metal push toward $15,000 per tonne .

Operationally, copper miners are fighting a relentless war of attrition against geological decay. Between 2012 and 2022, the average mined copper head grade fell by 13.4% . This forces operators to drill, blast, haul, and process vastly greater volumes of rock to yield the exact same metal output, fundamentally altering the stripping ratios and capital intensity of the mines . Total Cash Costs (TCC) are forecast to rise 3.3% through 2026, peaking at $32.24 per tonne . This strain is evident at tier-one assets: BHP’s Escondida project anticipates unit costs of $1.20–$1.50/lb, while the massive Grasberg operation in Indonesia has seen its return to a low-cost profile delayed to 2027 following operational incidents and phased ramp-ups . Despite these acute cost pressures, more than 99% of global copper production remains highly profitable, sitting safely below the 2026 consensus price .

Bulk Commodities and Battery Metals: The Deflationary Shock

While copper and precious metals thrive, iron ore, lithium, and nickel face a fundamentally different reality characterized by severe oversupply. The global nickel market remains saturated, with the average nickel AISC forecast to rise 3.9% in 2026 to $5.89/lb . Though the consensus nickel price of $7.49/lb provides a 21.4% AISC margin, producers are highly vulnerable to localized cost shocks or demand deterioration .

In the iron ore sector, the market is bracing for a massive deflationary shock originating from West Africa. The anticipated entry of the Simandou project in Guinea—boasting unprecedented scale and extremely high-grade hematite output—is poised to entirely redraw the global cost curve . With forecast benchmark prices slipping below $97/dmt, margins for high-cost producers globally will be severely compressed . Canadian concentrate producers (projected AISC of $99.80/dmt) and domestic Chinese concentrate producers ($79.94/dmt) will find themselves operating perilously close to, or below, the break-even threshold, likely forcing marginal producers out of the market entirely as Simandou’s low-cost supply floods global steelmaking supply chains .

| Commodity Sector | 2026 Cost Drivers & AISC Trends | Market Outlook & Pricing Dynamics |

| Gold & Silver | Silver AISC rising 3.8% globally to $23.44/oz, with severe regional variance (Mexico vs. Poland). | Banner year; safe-haven demand and central bank purchasing vastly outstripping inflation constraints. |

| Copper | TCC rising 3.3% to $32.24/t. Geological decay (13.4% head grade drop over a decade) forcing higher volumes. | Highly profitable. Driven by AI data centers, grid modernization, and structural 15% deficits by 2035. |

| Iron Ore | Simandou project entry acting as a massive deflationary force on the global cost curve. | High-cost producers (Canada, China) face severe margin compression as benchmark prices dip below $97/dmt. |

| PGMs | Platinum AISC rising 7.7% to $1,006.14/oz. Relief from Eskom power stabilization in South Africa. | Favorable. Less than 1% of production operating at a loss, a stark improvement from 2024. |

| Nickel & Lithium | Nickel AISC rising 3.9% to $5.89/lb. | Bearish. Sustained oversupply keeping prices compressed, limiting equity upside. |

Table 1: Summary of 2026 Commodity Cost Curves and Market Dynamics.

Major Equities: Consolidation, Capital Discipline, and Operational Synergy

The major diversified mining houses are responding to the policy-driven cycle and inflationary environment by prioritizing strict capital allocation frameworks, securing dominant copper exposure, and maximizing existing infrastructure through unprecedented joint ventures. The market valuation of these mega-cap equities heavily reflects their underlying commodity mix and their exposure to the energy transition.

| Symbol | Price | Change | % Change | Prev Close | |

|---|---|---|---|---|---|

| BHPBHP Group Ltd | $84.40 | +33.89 | +67.10% | $88.93 | |

| RIORio Tinto plc ADR Common Stock | $103.69 | +41.05 | +65.53% | $109.59 | |

| VALEVale SA | $16.32 | +6.52 | +66.53% | $16.58 | |

| FCXFreeport-McMoRan Inc | $63.01 | +24.99 | +65.73% | $66.12 |

Major Diversified Mining Equities Snapshot

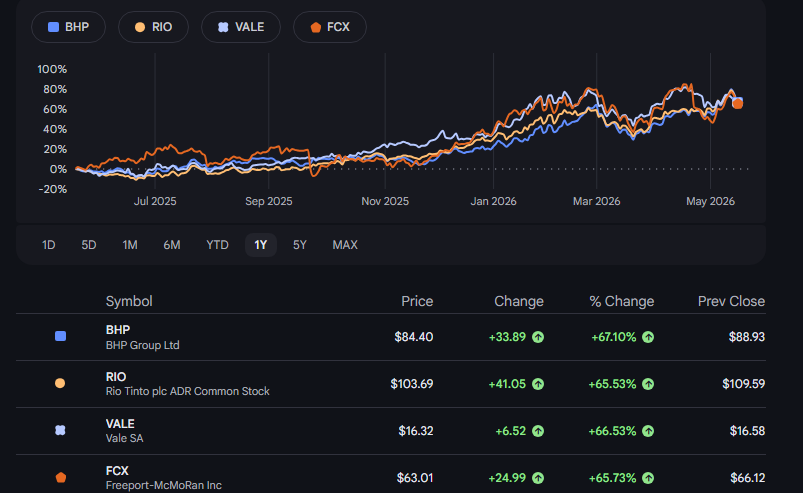

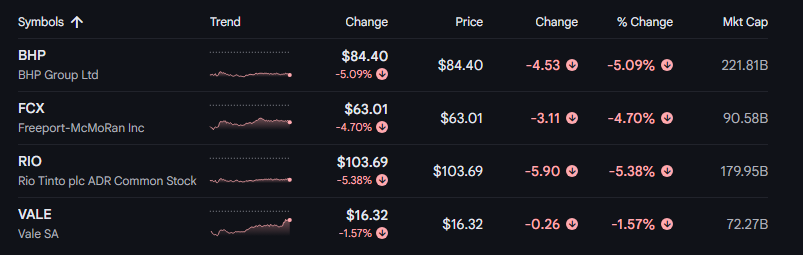

BHP Group (NYSE: BHP)

BHP has benefited immensely from its significant copper division, with its stock approaching 52-week highs in mid-2026, trading near the $84 level . The company is actively capturing a new wave of international generalist investor capital that is buying into the stock specifically to gain secondary exposure to AI-driven grid expansion . Management has maintained strict capital discipline, ensuring a minimum dividend payout ratio of 50% of underlying attributable profit . Despite headline legal headwinds—such as a UK court rejecting its appeal regarding the catastrophic 2015 Brazil dam collapse—the company’s broadly diversified commodity exposure provides a resilient defense against isolated sector slumps .

Rio Tinto (NYSE: RIO)

Rio Tinto, trading near $103, remains deeply reliant on its Pilbara iron ore operations, though it is aggressively ramping up copper output at its Oyu Tolgoi underground mine in Mongolia (which saw a 9% production increase in Q1) . Anticipating the margin squeeze from new African iron ore supply, Rio Tinto has pursued drastic cost-cutting measures. CEO Simon Trott has initiated a $650 million productivity and savings initiative, which includes reports of slashing up to 20% of the company’s Perth white-collar workforce . Concurrently, the company faces labor disputes, including a voted strike action at its Tiwai Point aluminum smelter in New Zealand . Analyst sentiment remains highly divided on the stock, with a consensus price target hovering near $101.75, reflecting the tension between its strong copper growth and vulnerable iron ore base .

The Pilbara Collaborative Blueprint

To aggressively defend their iron ore margins from rising capital costs, Rio Tinto and BHP have executed a historic strategic partnership in Western Australia’s Pilbara region. The two giants have signed non-binding Memoranda of Understanding to collaboratively mine up to 200 million tonnes of iron ore by sharing infrastructure across their neighboring Yandicoogina and Yandi operations . Under the agreement, BHP will supply its Yandi Lower Channel wet iron ore to Rio Tinto for processing at Rio’s existing wet plants . By leveraging existing infrastructure and eliminating the need for redundant, multi-billion-dollar capital expenditures to build new facilities, the majors are demonstrating a new blueprint for operational synergy . This capital-light approach extends the life of legacy operations and unlocks previously stranded resources located on shared tenure boundaries .

Freeport-McMoRan (NYSE: FCX)

Freeport-McMoRan represents the premier pure-play copper and gold equity among the large caps. Trading near $66, the company boasts a market capitalization exceeding $90 billion . Despite being forced to reduce its 2026 and 2027 production targets due to delayed timing for the Grasberg restart, FCX delivered a massive Q1 2026 adjusted EBITDA of $2.5 billion, easily beating BMO Capital’s $2.0 billion estimate . Analysts maintain a highly bullish outlook on the equity, with an average price target of $68.93 and high estimates reaching $76.00, citing the company’s unparalleled leverage to structural copper deficits and the safety of having more than 75% of its production located outside of Indonesia .

Vale S.A. (NYSE: VALE)

Vale remains the relative laggard among the majors, trading near $16.50 . Heavily exposed to iron ore and nickel—both markets facing severe oversupply and margin compression—Vale’s consensus estimates are notably cautious . Analysts maintain an average price target of $17.01, representing a modest upside, though downward revisions in both 2026 and 2027 earnings per share (EPS) estimates reflect the broader macroeconomic headwinds facing its core commodities . The company’s nickel sensitivities are currently modeling copper at roughly $12,660/t and cobalt hovering near $50,000/t, figures that will require sustained global industrial demand to justify .

| Major Miner | Core Focus & Growth Catalyst | Key Vulnerabilities / Headwinds | Consensus Stance (May 2026) |

| BHP | Copper expansion; AI/Grid electrification tailwinds; Pilbara infrastructure synergy. | Legacy legal risks (UK/Brazil rulings); exposure to soft metallurgical coal markets. | Moderately Bullish. Attracting generalist tech-adjacent capital. |

| Rio Tinto | Oyu Tolgoi copper ramp-up; drastic $650M cost-cutting initiatives. | High reliance on iron ore pricing; workforce strikes; mass white-collar layoffs. | Neutral/Divided. Consensus target ~$101.75. |

| FCX | Premier pure-play copper/gold exposure; massive Q1 cash flow generation. | Grasberg restart delays; rising input costs in North American assets. | Highly Bullish. Average target ~$68.93 with upside potential. |

| Vale | Leveraging mature Brazilian asset base; structural improvements to balance sheet. | Severe exposure to oversupplied iron ore and nickel markets; downward EPS revisions. | Cautious/Hold. Average target ~$17.01. |

Table 2: Strategic positioning and analyst consensus for top-tier mining equities.

The Anglo Teck Mega-Merger: Bypassing the Greenfield Bottleneck

The pursuit of scale and the desperation to secure long-life copper assets has culminated in the sector’s most defining M&A event: the mega-merger of equals between Anglo American and Teck Resources to form “Anglo Teck” . The new entity is explicitly designed to be a global critical minerals champion, headquartered in Vancouver, Canada, offering investors an unprecedented 70% exposure to copper .

Having secured Investment Canada Act approval and overwhelming shareholder support, the merger highlights a crucial industry reality: the capital requirements and permitting timelines for new greenfield mines have become so prohibitive that acquiring existing brownfield assets is the only viable path to rapid growth . The complex, multi-jurisdictional regulatory review—which has cleared Canada and Australia but remains in critical phases in the EU and China—demonstrates the immense bureaucratic friction inherent to modern resource consolidation . Nevertheless, the formation of Anglo Teck sets a precedent for how major entities will structure cross-border transactions to navigate long-term resource security in an increasingly polarized global economy .

The Junior Mining Ecosystem: Capital Flows and Market Psychology

If the major mining narrative of 2026 is one of consolidation, capital discipline, and defensive joint ventures, the junior exploration narrative is defined by a fierce competition for capital, extreme equity volatility, and an arms race of technological acceleration. Junior explorers—companies with no active mining revenue that exist solely to drill and prove resource deposits—operate at the most speculative edge of the capital markets.

Following a brutal, decade-long “funding winter” where risk capital aggressively migrated away from resource exploration and toward the technology and cryptocurrency sectors, 2026 has witnessed a dramatic, structural reversal . Between 2011 and 2023, the number of mining companies listed on the TSX Venture Exchange (TSXV) nearly halved as tech listings surged . However, driven by geopolitical uncertainties and the onset of a new commodity supercycle, capital rotation has returned to the resource sector . Trading volumes on the TSXV jumped to 47.5 billion shares early in the year, a massive 44.6% increase over the previous period .

Institutional and Retail Funding Metrics

The quantitative data from the global exchanges confirms this resurgence. In March 2026 alone, total financings raised on the TSXV spiked 481% compared to the previous year, with 161 individual financings executed . The primary Toronto Stock Exchange (TSX) welcomed three new mining issuers and facilitated over $2 billion in total financings in the same month . The Australian Securities Exchange (ASX) mirrors this buoyancy; new listings in 2025 raised $6.3 billion, a 54% increase and the highest since 2021, with secondary follow-on capital reaching $36.7 billion . Major ASX follow-on raises were dominated by resources, including massive tranches by companies like NXG ($600m) and ARU ($475m) .

In Canada, flow-through shares remain the lifeblood of the junior ecosystem. These tax-incentivized investment vehicles supply roughly three-quarters of all equity raised by eligible exploration companies . Extended by the federal government to bolster critical mineral security, flow-through financing effectively subsidizes the high failure rate of grassroots exploration, ensuring that early-stage drilling continues even when broader equity markets tighten .

The Psychology of Junior Equity Markets

The junior resources sector is intensely sensitive to macroeconomic monetary policy. Historical data establishes a firm correlation: falling Federal Reserve rate expectations coincide with significant outperformance in junior mining equities . Lower borrowing costs reduce the opportunity cost of holding highly speculative, non-yielding positions and exponentially increase the discounted Net Present Value of future mine cash flows . This creates a virtuous cycle: rising equity prices facilitate easier capital raises, leading to larger exploration budgets, which in turn generate discovery successes that further drive share price appreciation .

However, the market remains ruthlessly selective. While commodity-linked stocks attract speculative interest, grassroots explorers relying entirely on conceptual targets and serial dilution face acute funding squeezes . Inflation in drilling labor and contractor costs means exploration budgets yield significantly fewer meters drilled than a decade ago . Investors, battered by past cycles, now demand credible pathways to development and financing . Consequently, shifts in retail sentiment—amplified by the aforementioned AI investment biases—can produce violent daily price fluctuations. For example, micro-cap explorers like Pure Resources saw sudden 13.77% drops on generalized sentiment weakness, while others like Felix Gold experienced 150% annual rallies followed by sharp consolidation pullbacks .

Junior Exploration: M&A, Strategic Partnerships, and Technological Disruption

The junior market has fundamentally bifurcated. On one side are the advanced developers holding defined resources (Preliminary Economic Assessment or Pre-Feasibility Stage) in safe jurisdictions; on the other are grassroots explorers struggling for relevance. Because the capital required to build new processing infrastructure is prohibitive, the ultimate success metric for a junior in 2026 is securing a strategic partnership or outright buyout from a major producer .

The Shift to Strategic Partnerships

Rather than conducting greenfield exploration internally, mid-tier and major producers are outsourcing geological risk to the junior sector, stepping in to provide capital only once a resource is de-risked . This creates immediate value realization for the junior without the punishing equity dilution of open-market capital raises .

This dynamic is pervasive on the ASX. Mid-tier Australian gold producer Westgold Resources, which operates multiple processing hubs, executed a binding ore purchase agreement with junior New Murchison Gold . This allows the junior to mine its Crown Prince deposit and truck the ore 36 kilometers to Westgold’s facility, entirely bypassing the need to permit and build a proprietary mill . Similarly, commodity trading giant Trafigura provided up to US$50 million in prepayment financing alongside seven-year offtake agreements to Medallion Metals, drastically reducing the junior’s development capital requirements and time to first production . Other juniors, such as OzAurum Resources, have secured cornerstone investments from peer explorers to consolidate regional land packages .

M&A Premiums and Sector Consolidation

For juniors controlling proven, high-grade assets in stable jurisdictions, 2026 is a seller’s market characterized by substantial acquisition premiums. In the lithium sector, where critical minerals represent only 2% of funding allocation despite overwhelming transition demand, the scarcity of drill-ready projects creates massive premiums for juniors holding established resources .

In the precious metals space, M&A activity is robust:

- Gold Candle Ltd. & Fokus Mining: Gold Candle executed a $65 million all-cash takeover of Fokus Mining, offering a 36.8% premium to its VWAP, to instantly acquire 1.4 million ounces of inferred gold resources in Quebec’s Abitibi region .

- Heliostar Metals & Liberty Gold: Heliostar acquired the Goldstrike project for US$72.5 million, providing immediate value realization for Liberty’s shareholders through a structured buyout .

- Goldgroup Mining & Gold Resource Corp: A massive US$372 million business combination creating a new Mexican-focused precious metals producer, leveraging regional synergies .

Juniors that can leverage historical data from previous commodity cycles are particularly well-positioned. Magma Silver Corp, for instance, initiated a 4,000-meter drill program at its Niñobamba project in Peru, entirely directed by a historical US$7 million database compiled by Newmont Mining Corporation . By re-interpreting Newmont’s historical intersections (which included 72.3 meters grading 1.19 g/t gold), Magma saves years of preliminary expenditures, showcasing how modern juniors stand on the shoulders of past exploration megacycles .

Technological Disruption: AI and Drones in Exploration

The most critical differentiator for junior explorers in 2026 is the adoption of advanced technology. The days of blind grid-drilling are over. Junior miners are aggressively deploying artificial intelligence, satellite-based hyperspectral imaging, and autonomous drones to isolate targets before a single drill pad is cleared .

In highly prospective regions like the Arizona copper belt, the deployment of AI and drone technologies has reportedly tripled the rate of major porphyry discoveries . These technologies allow technical teams to analyze massive datasets of magnetic and gravimetric surveys in real-time, drastically reducing the amount of “dry holes” drilled . By accelerating the timeframe from initial survey to discovery, tech-driven juniors optimize their capital burn rate, command higher valuation premiums, and successfully attract tech-savvy family office capital that had previously abandoned the resource sector . Furthermore, strict adherence to Environmental, Social, and Governance (ESG) frameworks—facilitated by the low-impact nature of drone and satellite surveying—has transitioned from a marketing buzzword to a non-negotiable prerequisite for attracting institutional capital and securing government permits .

Future Projections and Strategic Imperatives

The exhaustive data surrounding the 2026 mining landscape yields several critical second and third-order insights that will shape capital allocation through the end of the decade. The consensus outlook dictates that the industry is no longer cyclical in the traditional sense; it is structurally bound to the imperatives of the energy transition, artificial intelligence infrastructure, and the geopolitical polarization of supply chains.

First, the politicization of mineral value means that jurisdictional safety now commands a premium that outweighs geological purity. A lower-grade, high-cost copper porphyry deposit located in Nevada or Ontario will consistently attract cheaper capital and higher M&A multiples than a high-grade equivalent in a non-allied or unstable nation. Western governments will continue to utilize defense acts and tax incentives to artificially subsidize the economics of domestic critical minerals, essentially underwriting the downside risk for domestic junior explorers.

Second, in an environment of 3.8% headline inflation and elevated borrowing costs, existing physical infrastructure has become the ultimate economic moat. The cost to construct greenfield mills, tailing dams, and deep-water ports has become so prohibitive that mid-tier and major miners will refuse to build them unless absolutely necessary. Therefore, junior explorers whose deposits sit within trucking distance of underutilized, legacy processing hubs will be acquired at vast premiums. Conversely, stranded, isolated discoveries—regardless of their size—may languish undeveloped for decades.

Finally, the relentless margin squeeze driven by declining ore grades and rising labor costs will force the industry into a paradigm of total automation. The efficiencies of traditional open-pit mining have peaked. To defend their margins, major operators will be forced to deploy massive capital toward fully electrified, automated, and mechanized underground bulk mining techniques, a transition already visible in operations like Grasberg.

Ultimately, the consensus outlook for mining stocks in 2026 is highly optimistic for entities that possess operational scale in copper and precious metals, and distinctly cautious for those exposed to bulk battery metals. For the junior sector, the return of speculative capital offers tremendous upside, provided investors meticulously target companies leveraging advanced AI exploration technologies and pursuing strategic partnerships that bypass the crippling capital expenditures of mine construction.